🧠 AMETEK (NYSE: AME): Quiet Compounder with 12% Upside

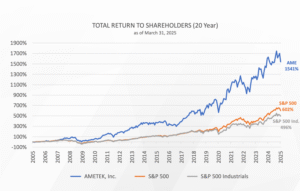

AMETEK delivers ~15% 5-year and +1,541% 20-year returns, outpacing S&P 500 through precision acquisitions, endorsed by value investor Francois Rochon.

Overview

Company: AMETEK, Inc. (NYSE: AME)

Analyst: Francois Rochon

Action: Buy

Forward P/E: ~29x

P/B: 4.1

Yield: 0.65%

Key Thesis

AMETEK grows earnings faster than the S&P 500 through precision acquisitions of niche industrial tech leaders. Its disciplined acquisition engine, diversified global presence (~50% non-U.S. sales), and operational excellence (26.6% operating margin) deliver consistent EPS growth (~7% YoY), high ROIC (10%+ by Year 3), and margin expansion.

Company Overview

AMETEK, Inc. (NYSE: AME) is a global leader in electronic instruments and electromechanical devices, with ~$7.0B in annualized sales across 150+ countries. Operating two segments—Electronic Instruments (EIG, ~75% of sales) and Electromechanical (EMG)—AMETEK serves mission-critical niches in aerospace, MedTech, semiconductors, and energy.

AMETEK Growth Flywheel

AMETEK’s growth is powered by a disciplined acquisition strategy. Since 2016, AMETEK deployed $8.1B across 33 acquisitions, targeting:

- Year 1: Cash accretive

- Year 3: 10%+ ROIC

- Exit: 20%+ selling profit within 3 years

Global & Sector Diversification

With ~50% of revenue generated outside the U.S., AMETEK isn’t overexposed to any single economy. Its structure provides built-in macro risk insulation.

| End Market | Exposure | Strategic Role |

|---|---|---|

| Aerospace & Defense | High | Mission-critical avionics |

| Medical & Healthcare | Rising | Robotic & surgical tech |

| Industrial Automation | Core | Motion control & vision |

| Semiconductors | Strategic | Optical metrology |

Valuation Metrics

~12% Upside

Premium Quality

Comp. vs Peers

Efficient Capital

Strong Balance Sheet

Funds Buybacks

Strategic Analysis

Strategic Summary: AMETEK is not just a manufacturer; it is a capital allocation machine. By acquiring niche players and plugging them into a global distribution and “Kaizen” efficiency network, they generate alpha.

Strengths

- Market Leadership: High-barrier products in aerospace, MedTech.

- Financials: $1.6B FCF, ~0.65x debt/EBITDA, $2.3B liquidity.

- Innovation: 26% sales from new products.

- Positioning: Dominant in niches too small for massive competitors to disrupt, but too complex for small players to enter.

Analyst Recommendation

Based on the “Quality Value” thesis by Francois Rochon, AMETEK represents a classic compounder. The current valuation (~29x Forward P/E) is a premium, but justifiable given the low risk profile, high recurring revenue, and proven M&A runway.

Verdict: BUY for long-term hold (3-5 years).

Key Takeaways

- Consistent Compounder: 15% annual returns over 5 years.

- M&A Machine: Disciplined strategy with proven ROIC targets.

- Defensive Moat: Niche markets with high switching costs.

- Upside: DCF suggests ~12% undervaluation despite premium multiple.