3 Stocks Bought by 4+ Top Funds in Q4 2024—Something’s Up!

Expert analysis on why Constellation Brands (STZ), Occidental Petroleum (OXY), and Domino’s Pizza (DPZ) are value investing gems

Unveiling Value: Why Top Funds Are Betting Big

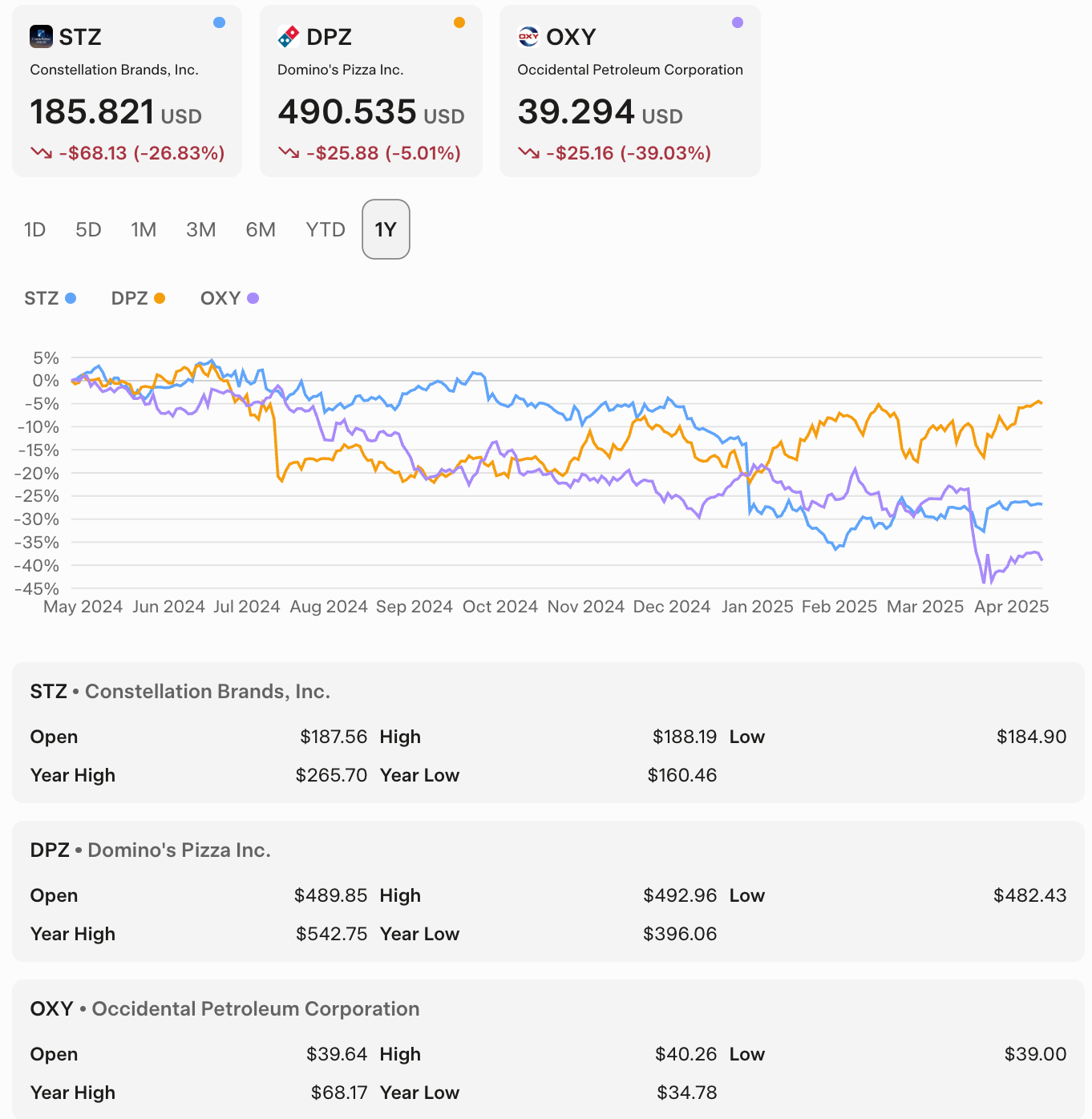

As disciplined value investors rooted in Benjamin Graham’s principles, we seek stocks trading below intrinsic value with strong fundamentals and a margin of safety. In Q4 2024, four elite value investing funds—Berkshire Hathaway, Baupost Group, Sequoia Fund, and Dodge & Cox—converged on three compelling stocks: Constellation Brands (STZ), Occidental Petroleum (OXY), and Domino’s Pizza (DPZ). The chart below compares the stock price performance of STZ, OXY, and DPZ in April 2025, highlighting their market trends.

Stock Price Comparison: STZ, OXY, DPZ (April 2025)

Below, we analyze these funds’ strategies, compare each stock’s key metrics to Consumer Discretionary sector averages, and integrate critical April 2025 news. Data is sourced from reliable platforms like Yahoo Finance and Investing.com.

Elite Value Investors: The Minds Behind the Picks

Berkshire Hathaway (Warren Buffett): Warren Buffett targets businesses with durable competitive advantages at undervalued prices. With $334 billion in cash, his Q4 2024 buys reflect precision, favoring consumer-driven and energy sectors for long-term compounding.

Baupost Group (Seth Klarman): Author of Margin of Safety, Klarman exploits market dislocations, buying undervalued assets with a risk-averse, opportunistic approach across diverse sectors.

Sequoia Fund: Inspired by Buffett, Sequoia pursues concentrated, long-term bets on companies with exceptional management and moats, driven by rigorous fundamental analysis.

Dodge & Cox: With a research-intensive, team-based process, Dodge & Cox seeks undervalued firms with growth potential, emphasizing resilience through extended holding periods.

Stock Analysis: Metrics vs. Consumer Discretionary Sector and Latest News

Constellation Brands Inc. (STZ)

![]()

Current Stock Price (April 30, 2025): $185.818

Business Overview: Constellation Brands leads the U.S. imported beer market with Corona, Modelo, and Pacifico (~82% of revenue), complemented by wine and spirits like Kim Crawford. In Q3 FY2025 (ended November 30, 2024), beer sales grew 4%, marking 59 consecutive quarters of depletion volume growth, driven by marketing and Mexican capacity expansion.

TTM P/E

49.24

Dividend Yield

2.18%

PEG Ratio

1.8

P/B Ratio

4.1

Operating Margin

31%

Free Cash Flow

$1.74B

Metrics vs. Consumer Discretionary Sector

| Metric | STZ | Sector Average | Insight |

|---|---|---|---|

| TTM P/E | 49.24 | 26.5 | 86% above sector, reflecting EPS volatility but premium brand value. |

| PEG Ratio | 1.8 | 2.5 | 28% below sector, offering growth at a compelling price. |

| P/B Ratio | 4.1 | 8.0 | 49% below sector, supporting intrinsic value. |

| Operating Margin | 31% | 10% | 210% above sector, reflecting superior efficiency. |

| Dividend Yield | 2.18% | 1.8% | 21% above sector, enhancing income appeal. |

Analyst Consensus

According to 19 analysts, STZ has a Buy rating with an average 12-month price target of $229.37, implying a 23.46% upside from the current price of $185.818 (April 30, 2025). High target: $260 (BMO Capital), low target: $180 (TD Cowen). StockAnalysis.com

Value Investing Perspective:

- Valuation Edge: STZ’s TTM P/E of 49.24 is high due to EPS volatility, but its PEG of 1.8 and P/B of 4.1 suggest value relative to growth and assets, justifying Buffett’s $990 million stake.

- Competitive Moat: Corona and Modelo’s dominance creates a brand moat with pricing power, aligning with Buffett’s and Sequoia’s quality focus.

- Financial Strength: A $3 billion capacity investment through 2028 and 31% operating margins signal robust demand and efficiency.

- Risks: Tariff risks on Mexican imports and immigration concerns could pressure margins, but Klarman’s Baupost sees a margin of safety in the current valuation.

Latest News (April 2025): Constellation Brands beat Q4 2025 earnings but issued a cautious outlook due to a 25% tariff on imported canned beer and aluminum cans, effective April 4, 2025. CEO Bill Newlands noted softer Hispanic consumer demand amid immigration policy concerns. The company announced a $200 million cost-saving restructuring and sold wine brands to The Wine Group.

Why Chosen: STZ’s brand strength, efficiency, and analyst optimism resonate with Buffett’s consumer focus, Klarman’s contrarian tariff play, and Sequoia/Dodge & Cox’s stability thesis. The tariff dip enhances its value entry point.

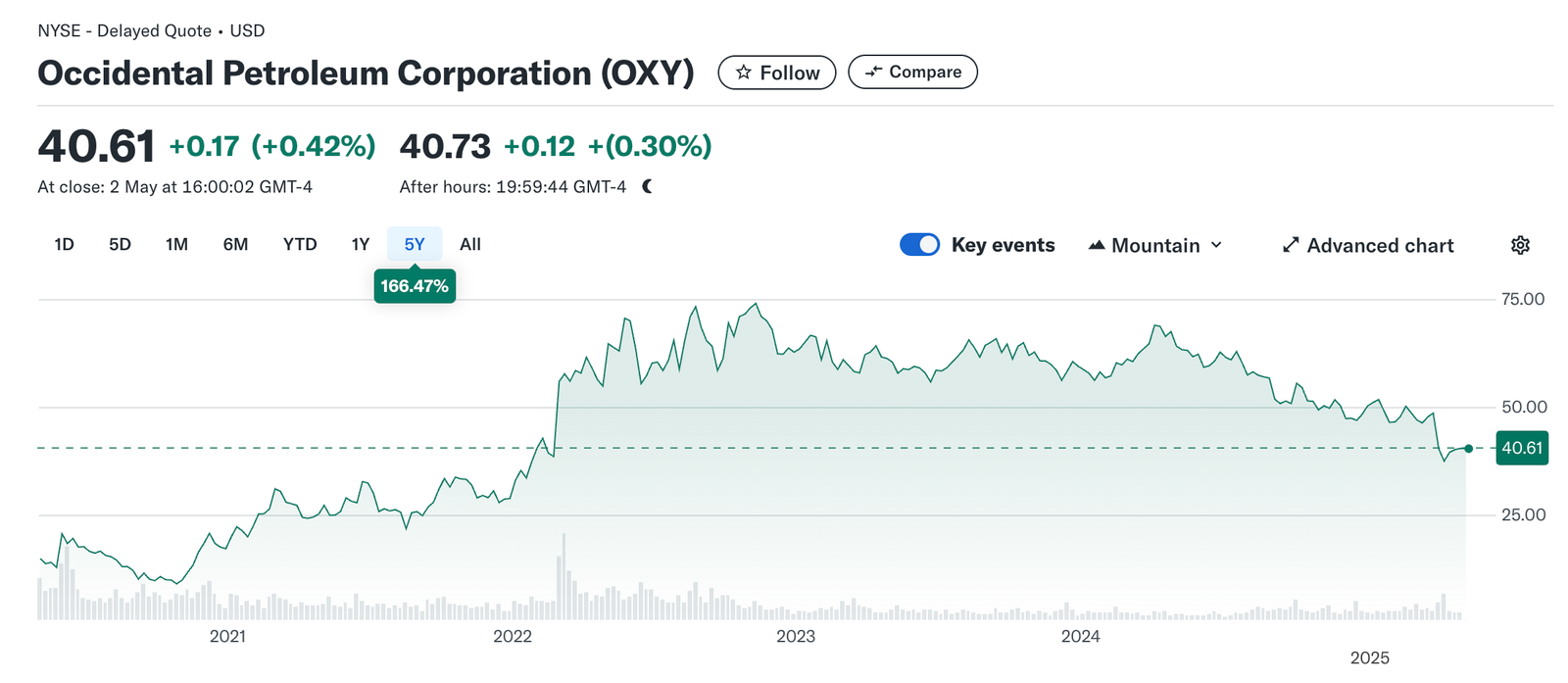

Occidental Petroleum Corp. (OXY)

![]()

Current Stock Price (April 30, 2025): $40.61

Business Overview: Occidental Petroleum is a leading oil and gas producer with Permian Basin dominance, enhanced by its $12 billion CrownRock acquisition. Its carbon capture and sequestration (CCS) initiatives position it for a low-carbon future. Q3 2024 saw $4.5 billion in debt reduction, boosting cash flows.

TTM P/E

10.73

P/B Ratio

2.1

Free Cash Flow

$1B

PEG Ratio

1.9

Operating Margin

25%

Dividend Yield

1.9%

Metrics vs. Consumer Discretionary Sector

| Metric | OXY | Sector Average | Insight |

|---|---|---|---|

| TTM P/E | 10.73 | 26.5 | 60% below sector, attractive post-19.8% April 2025 drop. |

| PEG Ratio | 1.9 | 2.5 | 24% below sector, signaling growth value. |

| P/B Ratio | 2.1 | 8.0 | 74% below sector, reinforcing asset value. |

| Operating Margin | 25% | 10% | 150% above sector, driven by low-cost production. |

| Dividend Yield | 1.9% | 1.8% | 6% above sector, enhancing income potential. |

Analyst Consensus

According to analysts, OXY has a Hold rating with an average 12-month price target of $54.19, implying a 37.81% upside from the current price of $39.333 (April 30, 2025). MarketBeat

Value Investing Perspective:

- Valuation Edge: OXY’s TTM P/E of 10.73, 60% below the sector’s 26.5, is compelling after a 19.8% April 2025 decline, backing Buffett’s 28.8% stake ($10.5 billion).

- Competitive Moat: Permian scale via CrownRock ensures low-cost production, a Buffett and Sequoia priority. CCS adds a future-proof edge.

- Financial Strength: CrownRock adds $1 billion in free cash flow at $70/barrel, with 2025 production at 1,385-1,445 Mboe/d. CCS targets a $3-5 trillion market.

- Risks: Oil price volatility and $18 billion debt remain, but deleveraging and $1M/well cost savings mitigate concerns.

Latest News (April 2025): OXY’s stock fell 19.8% in the past month, outpacing the sector’s 11.9% decline, due to commodity price volatility. Analysts like Scotiabank maintain a $40 price target despite a “Sector Perform” downgrade, citing Permian strength.

Why Chosen: OXY’s undervaluation and Permian dominance align with Buffett’s conviction, Klarman’s dip-buying, and Sequoia/Dodge & Cox’s CCS and cash flow optimism. The recent drop enhances its value appeal.

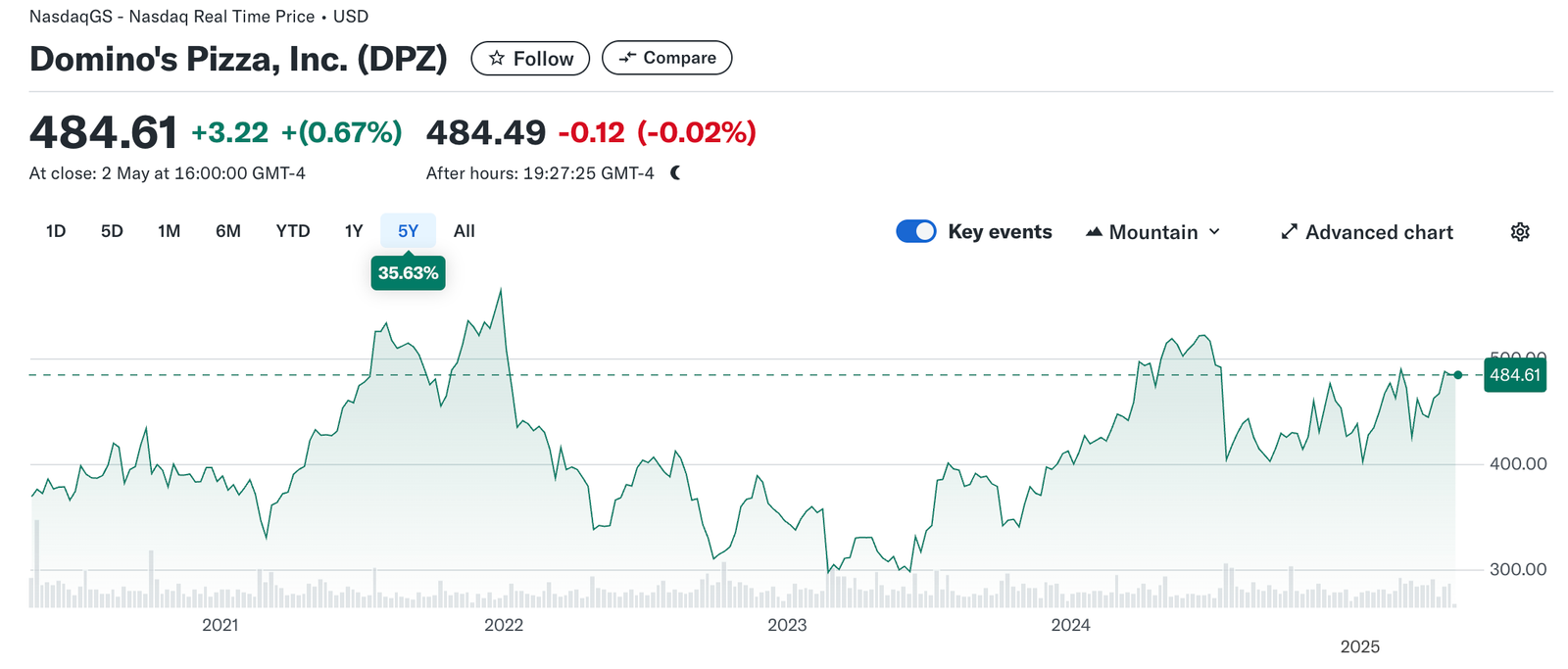

Domino’s Pizza Inc. (DPZ)

Current Stock Price (April 30, 2025): $492.414

Business Overview: Domino’s, the global pizza leader, operates 20,000+ stores with a franchise model and digital dominance (75% of orders). In Q4 2024, Berkshire boosted its stake by 86.5% (1.1 million shares), with 5.1% U.S. same-store sales growth via loyalty programs and tech.

TTM P/E

31.94

PEG Ratio

2.72

Operating Income

$617M

Operating Margin

17%

Dividend Yield

1.4%

Free Cash Flow

$497M

Metrics vs. Consumer Discretionary Sector

| Metric | DPZ | Sector Average | Insight |

|---|---|---|---|

| TTM P/E | 31.94 | 26.5 | 21% above sector, justified by 15% EPS growth forecast. |

| PEG Ratio | 2.72 | 2.5 | 9% above sector, reflecting premium for growth. |

| P/B Ratio | N/A | 8.0 | Negative book value due to debt, offset by cash flows. |

| Operating Margin | 17% | 10% | 70% above sector, reflecting franchise efficiency. |

| Dividend Yield | 1.4% | 1.8% | 22% below sector, balanced by buybacks and growth. |

Analyst Consensus

According to 28 analysts, DPZ has a Buy rating with an average 12-month price target of $505.36, implying a 2.63% upside from the current price of $492.414 (April 30, 2025). High target: $612 (Goldman Sachs), low target: $420 (Berenberg). StockAnalysis.com

Value Investing Perspective:

- Valuation Edge: DPZ’s TTM P/E of 31.94, 21% above the sector’s 26.5, is warranted by a 15% EPS growth forecast, appealing to Buffett’s quality focus.

- Competitive Moat: Digital innovation and a global franchise network create high barriers, aligning with Buffett’s and Sequoia’s cash-rich brand preference.

- Financial Strength: Q4 2024 revenue grew 6.2%, with $617 million in operating income. A 1.4% dividend and $500 million buybacks enhance value.

- Risks: Premium valuation and competition are concerns, but execution and partnerships mitigate risks.

Latest News (April 2025): Domino’s partnered with DoorDash on April 2, 2025, enabling delivery through DoorDash Marketplace starting May 2025 in the U.S., with Canada to follow. The stock rose 1.8%, reflecting optimism about expanded reach.

Why Chosen: DPZ’s cash flows and digital moat align with Buffett’s and Sequoia’s quality bias. Klarman sees a margin of safety in its consistency, while Dodge & Cox backs its growth. The DoorDash deal boosts its value-growth appeal.

Investment Implications for Value Investors

The convergence of Berkshire Hathaway, Baupost Group, Sequoia Fund, and Dodge & Cox on STZ, OXY, and DPZ in Q4 2024 signals compelling value opportunities. OXY offers deep undervaluation relative to the Consumer Discretionary sector, while STZ and DPZ’s premiums are justified by brand strength and growth. All three boast strong fundamentals and moats, from STZ’s brand power to OXY’s Permian assets and DPZ’s digital edge.

Actionable Strategy:

- Validate valuations using P/E, PEG, and P/B on Yahoo Finance.

- Assess moats: brand strength (STZ, DPZ) or assets (OXY) via Investing.com.

- Monitor risks: tariffs and immigration (STZ), oil prices (OXY), competition (DPZ).

- Adopt a 3-5 year horizon to capture intrinsic value, mirroring these funds.

These stocks carry risks, but their selection by top value investors, analyst optimism, and our rigorous analysis underscore their potential for long-term outperformance.

📈 📩 Get Alerts When Top Value Investors Buy

Build wealth by tracking top investors’ trades, rooted in strong fundamentals.

- 🔔 Instant Alerts: Catch undervalued stocks.

- ⏱️ Save Time: Skip deep research.